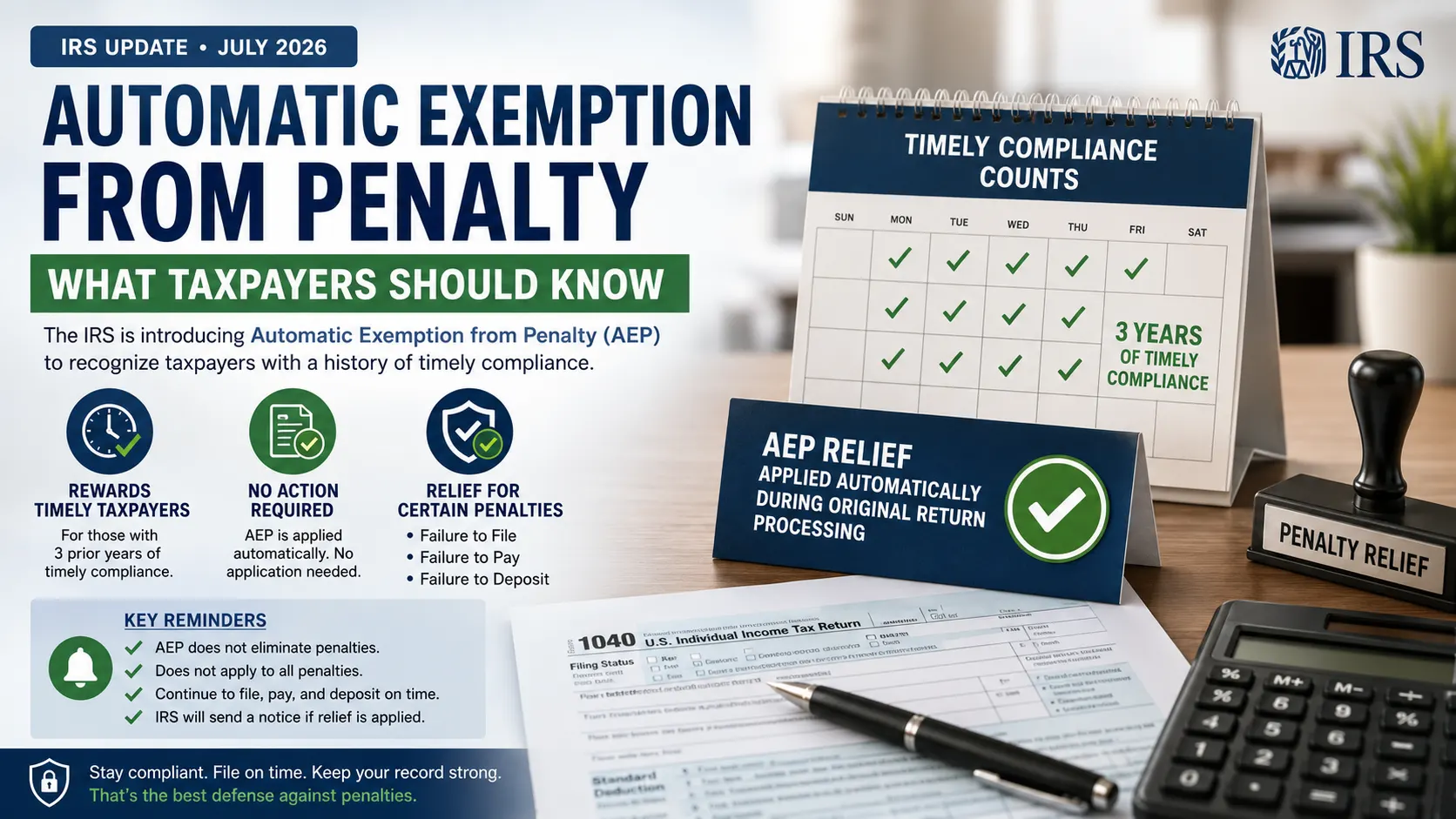

The IRS has introduced the Automatic Exemption from Penalty program to reward eligible taxpayers with three years of timely tax compliance. The relief applies automatically during original return processing for certain penalties, with no application or separate request required.

IRS Launches Automatic Exemption from Penalty for Taxpayers With Strong Compliance History

The IRS has announced the Automatic Exemption from Penalty program, also called AEP, to recognize taxpayers who consistently meet their federal tax obligations. Automatic Exemption from Penalty helps eligible taxpayers avoid certain penalties during original return processing after a one time compliance issue. The relief is automatic for qualified taxpayers, and no application or request is required.

The new policy, explained in IRS Fact Sheet FS-2026-12 released in July 2026, rewards taxpayers who have maintained a strong record of filing, paying, and making required tax deposits on time. While the program provides relief in certain situations, taxpayers must continue filing tax returns, paying taxes, and making deposits by the required deadlines.

Also Read: IRS Urges Taxpayers to Get Free Identity Protection PIN to Prevent Tax Identity Theft

What Is the Automatic Exemption from Penalty?

The Automatic Exemption from Penalty is a new IRS penalty relief program designed for taxpayers with a history of timely compliance. Instead of requiring taxpayers to request relief, the IRS automatically reviews eligibility while processing an original tax return.

If the taxpayer qualifies, certain penalties are not assessed. The IRS then sends a notice explaining that the penalty was removed because of the taxpayer’s previous compliance history.

The program rewards taxpayers who generally follow tax rules but experience a single compliance issue.

Why the IRS Created the Automatic Exemption from Penalty

The IRS created Automatic Exemption from Penalty to recognize taxpayers who consistently meet their tax responsibilities.

Many taxpayers file and pay on time year after year. Occasionally, unexpected situations can lead to one late filing, payment, or deposit. Rather than requiring these taxpayers to request penalty relief, the IRS now reviews eligibility automatically.

The goal is to:

- Reward long term compliance.

- Reduce paperwork.

- Make penalty relief more consistent.

- Speed up return processing.

- Reduce unnecessary requests for penalty relief.

How Automatic Exemption from Penalty Works

The Automatic Exemption from Penalty applies during original tax return processing.

The process is simple.

- The IRS processes an original return.

- The IRS reviews the taxpayer’s compliance history.

- The IRS checks all AEP eligibility rules.

- If qualified, certain penalties are not assessed.

- The taxpayer receives an IRS notice confirming the relief.

No application, phone call, letter, or online request is needed.

Penalties Covered by Automatic Exemption from Penalty

The IRS limits AEP to specific penalties.

Eligible penalties include:

- Failure to file penalties.

- Failure to pay penalties.

- Failure to deposit penalties.

Only these penalties may qualify under Automatic Exemption from Penalty when all IRS requirements are satisfied.

Eligibility Requirements

Taxpayers must meet several requirements before receiving relief.

Key requirements include:

- Three prior years of timely compliance.

- Timely filing history.

- Timely payment history.

- Timely tax deposit history when required.

- Eligible original tax return.

The three year compliance history is one of the most important requirements.

Eligibility Requirements at a Glance

| Requirement | IRS Requirement |

|---|---|

| Application Required | No |

| Automatic Review | Yes |

| Three Prior Years of Timely Compliance | Required |

| Original Return Processing | Required |

| IRS Notice Issued | Yes |

| Available for Every Penalty | No |

What Happens After Approval?

When Automatic Exemption from Penalty applies, the taxpayer does not need to contact the IRS.

Instead, the IRS will:

- Remove the eligible penalty before assessment.

- Process the return normally.

- Send a notice explaining the relief.

- Confirm the penalty was not assessed because of prior timely compliance.

The notice serves as official confirmation that the taxpayer qualified.

Penalties Not Covered by AEP

Many taxpayers assume every IRS penalty qualifies. That is not correct.

The Automatic Exemption from Penalty does not apply to every penalty under federal tax law.

Examples include:

- Daily Delinquency penalties.

- Accuracy related penalties.

- Information return penalties.

- Other penalties outside the AEP program.

Taxpayers remain responsible for all filing, payment, reporting, and deposit requirements.

Comparison of Covered and Non Covered Penalties

| Covered by AEP | Not Covered by AEP |

|---|---|

| Failure to File | Daily Delinquency |

| Failure to Pay | Accuracy Related |

| Failure to Deposit | Information Return Penalties |

| Eligible Original Return Penalties | Other Non Covered Penalties |

No Action Required From Taxpayers

One of the biggest changes under Automatic Exemption from Penalty is that taxpayers do not need to apply.

Unlike several previous IRS relief programs, AEP works automatically.

Taxpayers do not need to:

- Complete a form.

- Write a request letter.

- Call the IRS.

- Submit additional documents.

- Hire a representative.

If eligible, the IRS applies the relief automatically.

AEP Is Not Available for Every Late Return

Filing late does not automatically qualify a taxpayer.

The IRS clearly states that Automatic Exemption from Penalty applies only when every eligibility requirement is met.

Important reminders include:

- Late filing alone does not qualify.

- Late payment alone does not qualify.

- Three prior years of timely compliance remain essential.

- Eligible return types only qualify.

- The IRS reviews every case individually during processing.

Transition From First Time Abate

The IRS is replacing the long standing First Time Abate program over time.

During the transition period, First Time Abate remains available for:

- Eligible 2024 tax year returns.

- Eligible 2025 quarterly returns.

- Eligible 2025 tax year returns processed before AEP begins.

- Eligible 2026 quarterly returns processed before AEP begins.

Unlike AEP, taxpayers must request First Time Abate.

First Time Abate and AEP Comparison

| First Time Abate | Automatic Exemption from Penalty |

|---|---|

| Taxpayer requests relief | Relief applied automatically |

| IRS review after request | IRS review during processing |

| Limited transition period | Permanent replacement beginning with qualifying returns |

| Contact IRS required | No taxpayer action required |

When First Time Abate Ends

For original tax returns with due dates beginning January 1, 2027, First Time Abate will no longer be available.

The Automatic Exemption from Penalty will replace it for qualifying returns.

Taxpayers should continue following IRS filing deadlines because AEP does not remove every penalty.

Other Penalty Relief Options

Not every taxpayer qualifies for AEP.

If taxpayers do not qualify, other options may still exist.

Possible alternatives include:

- Requesting reasonable cause penalty relief.

- Appealing an IRS penalty relief decision.

- Providing supporting documentation if required.

The IRS reviews these requests separately from AEP.

Why Timely Compliance Still Matters

Some taxpayers may believe AEP removes the need to file or pay on time.

The IRS says this is incorrect.

Taxpayers should continue to:

- File tax returns on time.

- Pay taxes by the due date.

- Make required deposits.

- Submit required reports.

- Keep accurate tax records.

The Automatic Exemption from Penalty rewards past compliance. It does not replace current filing responsibilities.

Key Facts Every Taxpayer Should Remember

The IRS highlights several important facts.

- AEP is automatic.

- No application is required.

- Only certain penalties qualify.

- Three years of timely compliance are generally required.

- The IRS sends a notice when relief is granted.

- Filing and payment deadlines still apply.

- Not every taxpayer qualifies.

- Other penalty relief options remain available.

What This Means for Individual and Business Taxpayers

The Automatic Exemption from Penalty gives eligible taxpayers a simpler way to receive penalty relief after a one time compliance issue.

Instead of requesting relief, qualified taxpayers receive it automatically during original return processing. This reduces paperwork while recognizing taxpayers who have consistently followed federal tax rules.

Businesses and individuals should continue maintaining accurate records and meeting every filing deadline to remain eligible for future relief.

FAQs

What is the Automatic Exemption from Penalty?

The Automatic Exemption from Penalty is an IRS relief program that automatically prevents certain penalties from being assessed during original return processing. Eligible taxpayers generally need three prior years of timely compliance and do not need to submit an application or request.

Which penalties qualify under the Automatic Exemption from Penalty?

The program may apply to failure to file, failure to pay, and failure to deposit penalties. It does not cover every IRS penalty. Daily Delinquency penalties, accuracy related penalties, information return penalties, and several other penalties remain outside the program.

Do taxpayers need to apply for Automatic Exemption from Penalty?

No. Eligible taxpayers do not need to complete forms, contact the IRS, or submit requests. The IRS automatically reviews eligibility during original return processing and sends a notice if penalty relief is granted under the program.

Does Automatic Exemption from Penalty replace First Time Abate?

Yes, but only after the transition period. First Time Abate remains available for certain eligible returns processed before AEP begins. For original returns due on or after January 1, 2027, AEP replaces First Time Abate for qualifying taxpayers.

Can taxpayers still receive penalty relief if they do not qualify for AEP?

Yes. Taxpayers who do not meet AEP requirements may still request penalty relief based on reasonable cause. They may also appeal an IRS decision if they believe the penalty relief determination was incorrect under existing IRS procedures.

Does Automatic Exemption from Penalty remove the need to file taxes on time?

No. Taxpayers must continue filing returns, paying taxes, making required deposits, and meeting reporting deadlines. AEP only prevents certain penalties from being assessed for qualified taxpayers and does not eliminate normal tax responsibilities under federal law.

Conclusion

The Automatic Exemption from Penalty gives eligible taxpayers automatic relief from certain IRS penalties after a one time compliance issue. The program rewards taxpayers with a strong history of timely filing, payment, and tax deposits while reducing the need to request penalty relief.

Taxpayers should continue meeting every filing and payment deadline because AEP applies only to qualified returns and specific penalties. Maintaining a consistent compliance record remains the best way to qualify for future relief.

Leave a Comment